In over-the-counter markets — like the bond world — traders have historically needed to pick who to contact to get quotes and trade, versus simply routing an order to an exchange.

Trading relationships are therefore continually established, nurtured, and churned with the merry go round of personnel movements. Traders prefer counterparties they trust — and even more saliently, ones they like.

In theory, dealing with a small group of counterparties limits information leakage: your trade request might be a valuable signal, foretelling a market move. When Warren Buffett buys a stock, he values discretion — it would be foolish to broadcast his intent to everyone and risk driving the price against him.

But too much discretion can often be foolish. Asking 2 dealers for a quote will often result in inferior pricing vs asking 100 dealers simultaneously. Traders therefore need to optimize how many parties they interact with depending on the nature of the trade – and generally default to a small trusted set.

This optimization has fueled lavish spending to influence decision makers steering billions of trade flows. Enter the Peter Luger dinners and box seats at MSG — brokers to traders, traders to clients, clients to LPs. It’s all about building that relationship and affinity for your counterparty.

But here’s the reality: the vast majority of trades today are small tickets with no market-moving informational value. They are part of a sea of electronic flows from brokerages, advisors, and asset managers managing inflows, outflows, and rebalancing. Only ~5% of volume represents true alpha-seeking and warrants the specialized “work it quietly” workflow.

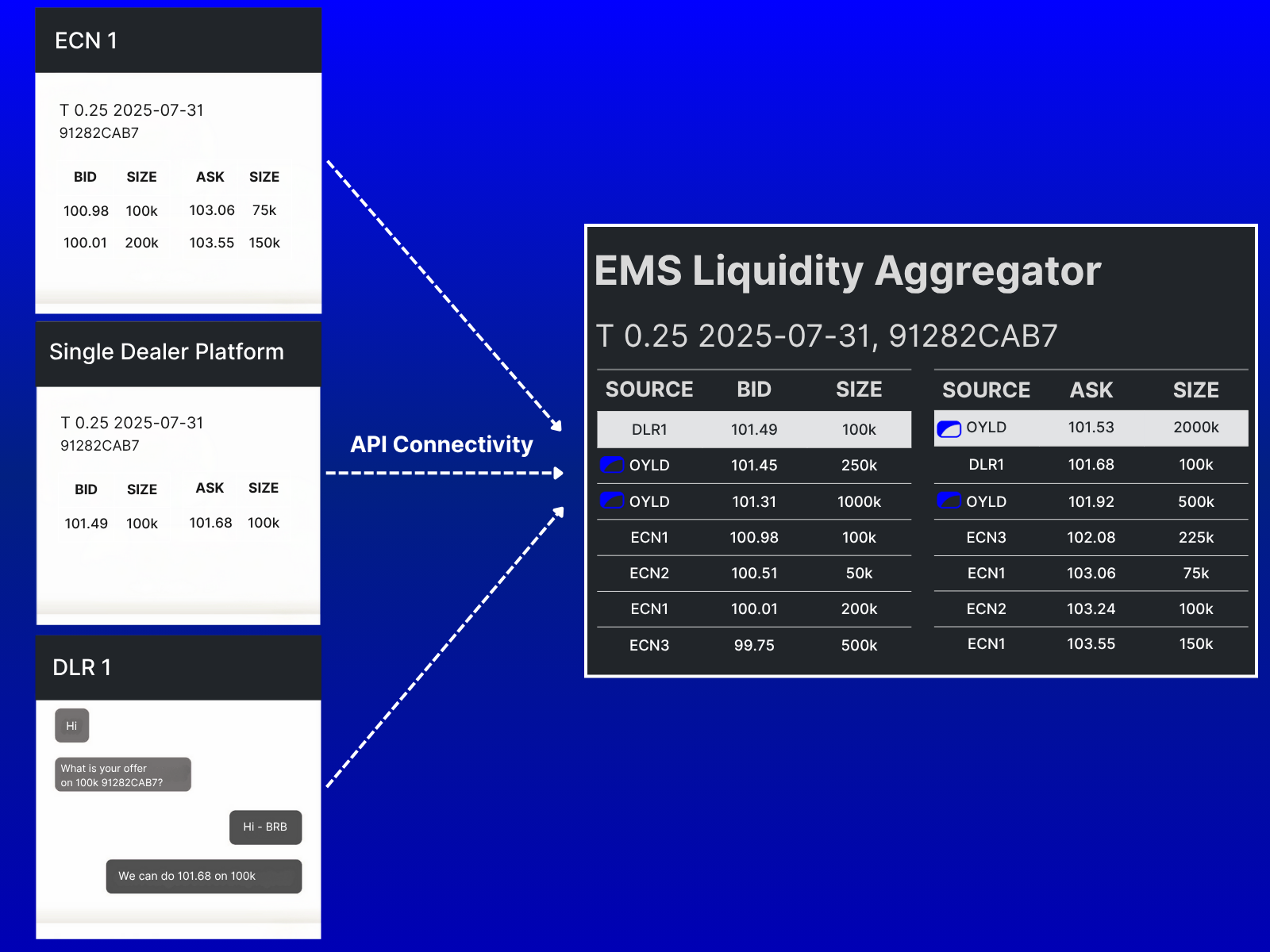

These flows are increasingly being handled by systematic processes. As FI is electrifying, dealers and venues are publishing quotes throughout the day. Clients are developing liquidity aggregators to ingest the quotes, and then route orders destinations with the best price.* The trade router logic is harder to influence with Wagyu from Nobu and ski trip to Aspen, and doesn’t complain about needing to compare 100 quotes instead of 2 as inputs. It obediently follows the algorithm: choose the best price.

I’m often asked why a client would trade with OpenYield — often by intelligent people within the industry. The question reveals the entrenched old-school mentality of preferring counterparties you like. The people asking do not fully appreciate the rise of the new school systematic engines, and are only faintly familiar with the national market system established in equities decades ago (equity colleagues are on different floors).

To answer, they are not trading with us because we spent our precious equity capital ferrying their reps in a chopper to Winged Foot for the back nine, or because we chuckled with their execution traders while clinking glasses of Louis XIII.

The answer is simpler: clients trade with us when we show the best price in competition. Anything else — any other behavior — violates the very objective of best execution. It smacks of rent-seeking behavior – and it is not long for this world.

The relationships between parties still matter, but are morphing from tactical trader banter to strategic dialogues to build better systems and products. Trust and collaboration with our subscribers are the lifeblood for our roadmap.

In an increasingly electronic world, best price wins. Fortunately for the luxury entertainment industry, there seem to always be more opaque markets where ambitious operators have a need to establish trusted relationships. For the bond market, growing pre-trade transparency and automated routing rules are rewriting the expenses required to maintain trading. Value is returned to the investor bottom lines, and the gears of efficiency continue their inevitable grind through capital markets.

Jon

* Dealers and venues disseminate indicative prices that are increasingly reliable