“Without data, you’re just another person with an opinion,” W. Edwards Deming

The move to firm and transparent bond-market liquidity has been glacial when compared to other asset classes like equities, but it’s starting to take off. Part of that transition is due to a drive towards transparency across asset classes through electronification, and importantly, greater adoption of ATS trading, and away from bilateral dealer markets, across fixed income asset classes, Although ATS trading is entrenched and expanding across the TRACE-eligible universe,1 progress to overtake interdealer and dealer-to-customer markets is happening, but not overnight.2

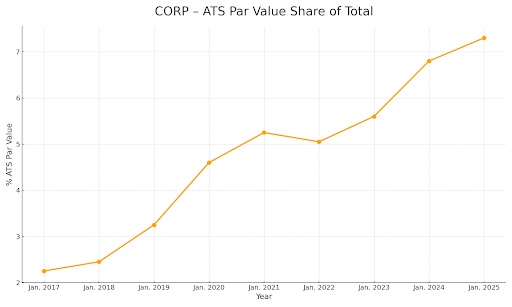

Still, taking a longer lens, it’s clear that ATS adoption is trending up. A look at year-over-year monthly snapshots for the corporate and agency markets (as a percentage of overall activity), reveals momentum in favor of structural change.3 The chart below is a good case for the evolutionary growth of fixed income markets, insofar as it demonstrates momentum in favor ATS-driven trading venues, arguably aided by the COVID pandemic era (circa late 2019 to early 2023).

And as the bond market electronifies, there is cause for optimism that future growth will continue to accelerate, fueled by complimentary structural factors. Examples include a move away from captive execution via clearing arrangements, firms gravitating from GUI-driven trading to API-based connectivity, and the adoption of algorithmic strategies and smaller trade sizes that have been commonplace in the equities markets for decades. We think this trend can gain even more traction with the adoption of newer electronic offerings like OpenYield to drive trading decisions based upon firm quotes, all-to-all connectivity, and no minimum trade sizes.

Across fixed income, additional structural complexities provide important context. Municipal markets provide an easy example; there are many issuers at all levels of state and local governments, and generally smaller issue sizes. And given their state-specific tax-exempt features, liquidity can be regional, with retail investors often holding issues to maturity. Even for more liquid securities like on-the-run corporates, highly decentralized trading ultimately acts as a drag on price discovery.

Less price transparency in indicative and decentralized markets introduces complexity for best execution decisions. And in this case, often means economic rent caused by these structural impediments, resulting in more expensive trading. To complicate matters further, FINRA Rule 5310 and MSRB Rule G-18 both present an industry-wide challenge to demonstrate that prices to clients reflect “reasonable diligence” so that they are as favorable as possible. The MSRB’s rules state that reasonableness will include “the information reviewed to determine the current market for the subject security or similar securities.”4 OpenYield features modern technology, purpose-built for easy diligence regarding the character of the market for the security.

A Deeper Dive Into The Regulatory Challenge

“Data is like garbage. You’d better know what you are going to do with it before you collect it.” Mark Twain

The quote is likely apocryphal, but it sure seems like something Mark Twain would say in a best execution discussion. And it’s not far off from what FINRA and the MSRB expect. Both regulators have common expectations of what would represent reasonable diligence in any best execution analysis, including:

- the character of the market for the security;

- the “number of markets checked,” and;

- the accessibility of quotations5

For each of these criteria, there are strong reasons to utilize a market like OpenYield, and the premise underlying these criteria is “connectivity.” We supply real-time depth of book of executable firm quotations via a vanilla FIX connection, and user-friendly GUI functionality.6 And further, with respect to the number of markets checked, FINRA Notice to Members 15-46, specifies that a firm should regularly consider execution quality “at venues to which it is not connected and assess whether it should connect to such venues.” Although ten years old, NTM 15-46 notes that with respect to fixed income securities, that:

pre-trade transparency, such as through electronic trading platforms, is also increasing in the fixed income markets, although predominantly for smaller orders, and firms need to routinely analyze and determine whether incorporating pricing information available from these systems should be incorporated into their best execution policies and procedures.

To be sure, connecting to venues like OpenYield to analyze prices and available liquidity is part of the brief. Incorporating available pricing from a modern and transparent marketplace like OpenYield is an easy avenue for good governance.

Tools and Technology

“The first thing you do when you get out to center field is put up your finger and check the wind chill factor, “ Mickey Rivers

While Mickey’s terminology was slightly off, patrolling center field in Yankee Stadium meant he had his head on a swivel. And in the case of best execution, taking on data, checking that ‘wind chill factor,’ means that connectivity initiatives cannot languish buried amongst technical deliverables. Consequently, “accessibility” includes having adequate technical resources to place orders with various venues to improve execution outcomes.

Regulators looking at best execution have from time to time taken the view in enforcement matters that checking other markets is reasonable diligence; fines for this activity can be steep. Noteworthy FINRA enforcement matters of recent vintage reveal large fines for not checking available venues, or too-high markups that might have been caught with better supervision.7 But by the time a case reaches an enforcement posture, it’s too late.

In the (blunt) words of the MSRB, “[a] dealer’s failure to maintain adequate resources (e.g., staff or technology) is not a justification for executing away from the best available market.”8 A transparent market like OpenYield means that informational disadvantages about liquidity sources are becoming far less of an obstacle to price discovery than in the recent past. Prioritizing best execution through the embrace of bond-market transparency is both a better business outcome, and sound regulatory governance.

Conclusion

“It is a capital mistake to theorize before one has data.” – Sherlock Holmes in “A study in Scarlet” by Arthur Conan Doyle

Best execution is tough enough, and across the fixed income landscape, the unique liquidity and price discovery challenges require a deeper understanding of the nature and sources of available liquidity. Incorporating information from transparent sources like OpenYield will drive better pre-trade analysis. And arguably, better pre-trade analysis will lead to easy (and satisfying) post-trade transaction cost analysis, yielding both investment and supervisory dividends.

With apologies to Matt Levine, we know that “people are worried about bond market liquidity” but we make no apologies about taking an innovative approach to providing transparency through firm, actionable quotes and modern API-first technology, coupled with low fees. As FINRA put it, firms have an obligation to consider “advances in trading technology and communications, and consider how these changes may afford new opportunities for more favorable executions for customer orders.” OpenYield’s modern architecture, low costs and all-to-all trading possibilities represent an important step for market participants navigating this evolutionary trend.

1 FINRA Rule 6710(a) contains additional detail, but for our purposes, the TRACE-eligible universe of products includes dollar-denominated fixed-income securities like treasuries and corporate debt, as well as agency securities. Notably, it does not include municipal securities or money-market instruments.

2 For more on these challenges, see these companion pieces from the OpenYield blog: Elevating Fixed-Income Trading: From “Fading” Quotes to Firm, Transparent Prices; and Best Price Wins in Transparent Markets.

3 Sourced from FINRA’s TRACE Monthly Volume Files, which can be found at: https://www.finra.org/finra-data/browse-catalog/trace-volume-reports/trace-monthly-volume-files

4 See MSRB Rule G-18(a)(4).

5 See FINRA Rule 5310(a)(1), and MSRB Rule G-18(a), respectively. There is other language in common between the respective rules; these are merely illustrative.

6 For more on the industry-wide regulatory challenge, see Best Execution and Fixed Income ATSs, from the OpenYield blog.

7 See, e.g., TradeStation Securities, Inc. (censure, $850,000 fine) and GlobalLink Securities (censure, $200,000 fine, $397,862.20 in restitution, and retention of an independent consultant).

8 See MSRB Rule G-18.02, “Maintenance of Adequate Resources.”

9 FINRA Notice to Members 15-46, at p. 12.