The Exodus to OTC

To appreciate why bonds are so gnarly to trade today as a retail investor, let’s rewind the clock 100 years to the Roaring Twenties. Imagine the scene: the New York Stock Exchange was bustling, with stocks and bonds traded side by side on the big board. Telephone clerks fielded orders, and the central limit order book dictated the price-time priority of executions. The *clack clack* of the ticker tape revealed trades (the literal prints), and investors of all kinds enjoyed the same prices – what a time to be alive! Academics comparing bond transactions in the 1920s to the modern landscape have shown that retail spreads became more expensive[1] despite the massive expansion in market size, participation and telecommunications. What in the world transpired?

Dual forces converged to transition volumes away from the exchange and toward the over-the-counter (OTC) market. First, retail equity trading volumes exploded during the bubble of the 1920s, leaving institutions with relatively higher participation in the bond market. While retail investors depended on exchanges for trading, institutional investors were able to go directly to dealers and leverage their relationships, which generally means using their larger size to negotiate better pricing trade by trade.[2] At the same time, the NYSE biased its scarce physical marginal resources toward stocks, as their take rate was higher. Consequently, bond liquidity dissipated on exchange and migrated to the OTC market, where it has remained to this day. By the time stocks reached a similar tipping point of institutional domination in the 1950s, the exchange introduced Rule 394, preventing members from trading away and cementing its position as the central venue for equity liquidity.[3]

The defining characteristics of OTC trading that benefited big institutions have harmed small retail investors. While institutions were able to exploit their size in direct dealer negotiations to obtain better pricing, retail investors could not, leaving them vulnerable to being exploited. Another key factor was information leakage. OTC trading is quiet, with no pre-trade or post-trade transparency. Institutions were sophisticated in knowing how to price securities and preferred to limit the footprint of their trading activity. This opacity hurts small investors, who have limited abilities to price securities and generally aren’t concerned about information leakage as their flows are not market-moving.

New World Order

Fast forward to today, and the world has changed: we may not have flying cars, but dealers now have the ability to electronically quote bonds. This shift toward automation means pre-trade transparency is increasingly common, as opposed to the days when quotes had to be communicated via phone or chat (“voice trading”). Post-trade transparency has increased due to regulatory reporting requirements. For corporate bonds, TRACE reporting emerged in 2002[4], while for municipal bonds, MSRB reporting emerged in 2005[5], both providing a public tape for post-trade transparency. Trades no longer remain in the dark.[6] Despite these significant market developments, the OTC paradigm has persisted as a market structure local equilibrium for nearly a century – but the pendulum is now swinging back to a centralized model.

The dominant electronic platforms that facilitate fixed income trading today were designed and crystallized during the rise of the internet. The institutional workflow of calling several dealers to collect quotes was replaced with the electronic “request for quote” (RFQ), which mimics the workflow and remains the primary convention for engagement today. To cater to the retail segment, the original Alternative Trading Systems (ATSs) emerged on the back of the internet to functionally match buyers and sellers – similar to an exchange, though regulated differently. An ATS displays an “order book” that is populated with indicative dealer quotes intended to solicit customer orders. Dealers can then optionally confirm their price, or counter with a revised price. Importantly, both RFQs and traditional ATS styles contemplate the manual nature of trading with a final human step to confirm trades. The key difference is that the classic RFQ is relationship-driven since customers choose which dealers to poll, while the ATS model is price-driven with quotes typically anonymous.

Institutional Decisions

Institutions have generally ignored ATSs given their relatively small volumes – they prefer direct trading with dealers. But the ATS share of the market is rising as both automated liquidity[7] and odd-lot demand is transforming the segment. Over the last 5 years, the share of muni customer trades executed on an ATS has doubled from 7.7% to 15%.[8] Similarly, for corporate bonds, the portion of ATS par value traded vs total customer flows has also doubled from 4.4% to 9.4% over the same period, hitting 234B in Q1[9].

The true ATS share of risk transfer is likely much higher as customer trades are often sourced via an ATS by a broker, and then risklessly back-to-backed into customer accounts (with a markup), which are tallied as additional trades.[10]

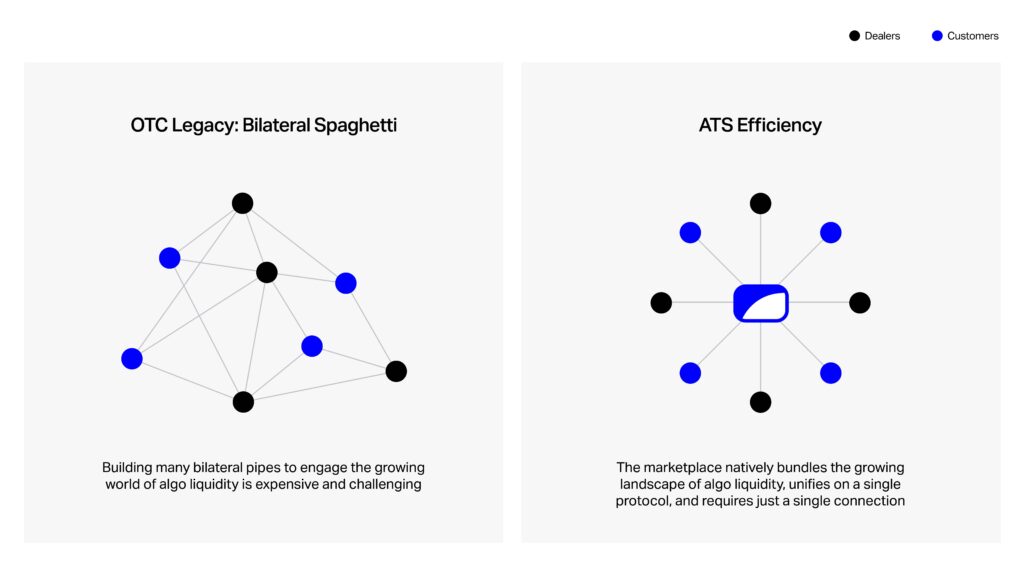

As automated liquidity continues to grow, larger institutional customers are being challenged to reassess their styles of engaging in the market. Their interest is fanned by general needs to scale trading operations with technology, and specific opportunities to leverage odd lots in their separately managed accounts (see Unwrapping the Fund). The traditional OTC mindset would suggest establishing direct electronic connections with the growing number of algo dealers, aggregating the disparate formats of liquidity and developing routing logic. In other words, BestEx Capital would have to maintain a dozen FIX connections to their favorite dealers, capture the flood of information internally into a trade system and send orders to one of those dozen dealers using logic to optimize for best execution. This is a significant undertaking, requiring non-trivial oversight to ingest and rationalize, as well as endless maintenance around new dealers and changes to various connection formats.[11]

The Power of the Marketplace

Fortunately, there is an alternative available: the marketplace! A centralized ATS aggregates the growing pool of algo liquidity, unifies it on a single protocol in real time and enables participants to trade via a single connection. Furthermore, access to the ATS unlocks connectivity to every participant, with all executions occurring using a consistent logic at a point in time such as price-time priority. On an ATS, liquidity can flow omnidirectionally, as any participant can rest orders, a capability that can be supported with tooling such as evaluated pricing. For players who prefer discretion, an ATS can also flexibly provide anonymity by serving as an intermediary.

The marketplace is destined to be the new equilibrium for interaction with automated liquidity. Attempting to replicate the value of the marketplace in the tradition of bilateral connections would be a road to expensive frustration.

Every mature market has a mix of OTC and exchange trading styles – stocks, options, even crypto – where trades that require conversations happen OTC (via conversation) and those that don’t print on marketplaces. The fixed income world has developed the technology to eliminate those conversations, and is now going through a behavioral shift – like a teen in the throes of puberty – to accept that many bond trades do not require human interaction. Consequently, liquidity is increasingly migrating back to centralized venues for transaction efficiency.

Liquidity will ultimately coalesce on the marketplaces that deliver the most value back to participants in the form of ease, cost, breadth and depth, resulting in an equilibrium that finally puts the retail investor back on a level playing field. At OpenYield, this is our north star. Welcome to the new Roaring Twenties!

[1] “The Microstructure of the Bond Market in the 20th Century” Bruno Biais, Richard C. Green, https://www.tse-fr.eu/sites/default/files/TSE/documents/doc/wp/2018/wp_tse_960.pdf

[2] Bond desks are generally optimized around servicing VIP customers

[3] Rule 394 https://www.sechistorical.org/collection/papers/1960/1960_Rotberg_RULE394.pdf

[4] FINRA About Trace: https://www.finra.org/investors/insights/what-is-TRACE#:~:text=About%20TRACE,for%20all%20eligible%20corporate%20bonds

[5] Muni Realtime Reporting Notice: https://www.finra.org/sites/default/files/NoticeDocument/p012856.pdf

[6] For US Treasurys, TRACE data is collected but not yet disseminated. This is actively being explored: https://www.sec.gov/news/statement/gensler-statement-finra-020724.

As of 2024 this data is still not yet disseminated to the public.

[7] Automated liquidity is anything non-negotiable. Can be driven by algos or humans.

[8] MSRB Report: https://www.msrb.org/sites/default/files/2022-08/MSRB-Customer-Trading-with-Alternative-Trading-Systems.pdf

[9] TRACE Volume Reports: https://www.finra.org/finra-data/browse-catalog/trace-volume-reports

[10] The ATS subscriber is the broker, who then “trades” the bond to the retail customer account with a commission as a separate trade. TRACE details here https://www.finra.org/filing-reporting/trace/faq#GeneralReporting

[11] Participants can outsource parts of this task to external vendors such as Execution Management Systems (EMS)

[12] Technical costs aside, customers are unable to trade directly with other customers without a broker in the middle. There is a growing pool of principal firms – non-BDs – that provide liquidity in fixed income markets.

© 2024 OpenYield Inc. Securities products and services are provided by OpenYield Trading LLC, member FINRA/MSRB/SIPC and wholly-owned subsidiary of OpenYield Inc.